The India-Middle East-Europe Economic Corridor (IMEC, or also known as IMEEC) is a proposed multinational infrastructure initiative aimed at upgrading connectivity between the three regions through integrated trade, energy, and digital networks. Announced at the Group of 20 (G20) Summit in New Delhi in September 2023, IMEC is envisioned partially as a counterweight to China’s international infrastructure project, the Belt and Road Initiative (BRI). The multinational initiative consists of two main segments: an Eastern Corridor linking India to the Persian Gulf and a Northern Corridor connecting the Gulf to Europe via the Levant and Mediterranean. Its multimodal infrastructure, including railways, deep-water seaports, electricity grids, and high-speed data cables, could potentially reduce shipping costs by billions and shipping times by up to 40%, compared to traditional routes. At present, however, the corridor in its original form is effectively on hold due to regional instability.

Former Secretary of State Antony Blinken championed the project as part of broader efforts to normalize relations in the region, building on the I2U2 framework (involving India, Israel, the United Arab Emirates, and the United States) and the Abraham Accords. However, just a month after IMEC’s announcement, the October 7, 2023, Hamas attack on Israel and the years of regional wars and turmoil it triggered divided key partners in the agreement — which hinges on Saudi-Israeli normalization, a credible pathway toward Palestinian statehood, improved Saudi-UAE relations, and a free flow of maritime traffic through the Strait of Hormuz — greatly slowing momentum. Thus, alternative transregional connectivity projects, including a Saudi-backed northward corridor through Syria or a Turkish-Iraqi route, are under discussion or in development.

Organization and Basic Elements of the Proposal

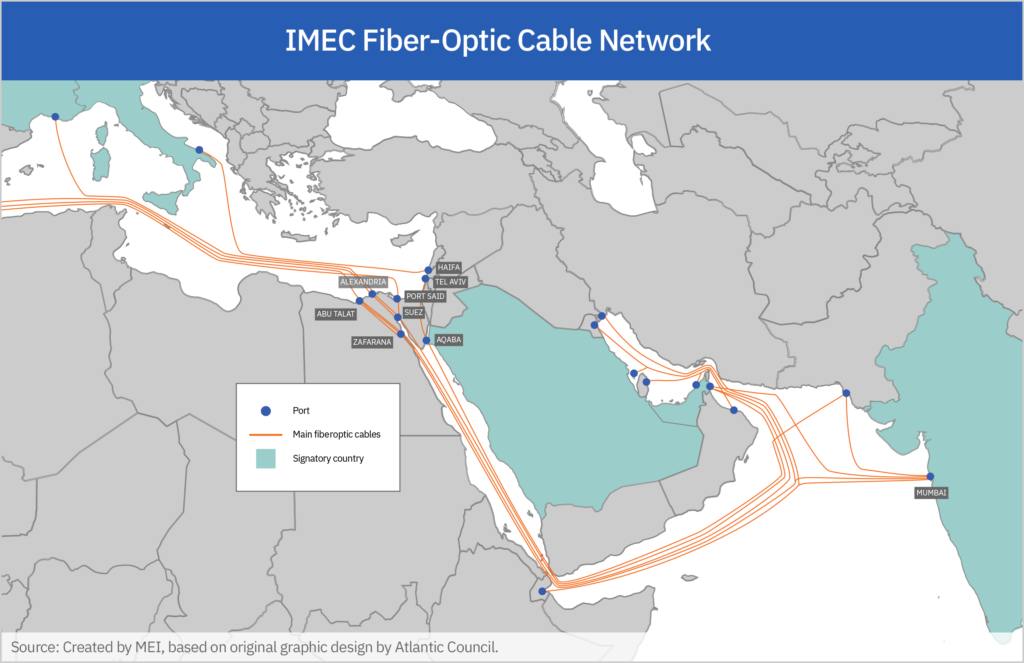

IMEC is designed to create a resilient supply chain network connecting South Asia (namely India), the Middle East, and Europe. It aims to transport goods, energy, and data, bypassing the Bab al-Mandab and Suez Canal. The corridor’s proposed infrastructure would include upgraded ports, integrated grids, rail links, and subsea cables, leading to a more efficient alternative trade, energy, and data route that advances the long-term interests of the United States in the region.

The core signatories are India, the US, the UAE, Saudi Arabia, Israel, Jordan, France, Germany, Italy, and the European Union. Notably absent are Qatar, Oman, Turkey, Iraq, and Iran.

The proposed corridor would address vulnerabilities in global trade routes exposed by events such as the 2021 Suez Canal blockage and Red Sea disruptions from Houthi militants starting in late 2023. It could cut transit times from India to Europe significantly and thus reduce costs by 30%. Although multimodal transportation connections form the corridor’s core, the lasting impacts from IMEC likely lie in the energy and technology sectors. Fiber-optic lines laid along the route would bypass the vulnerable data chokepoint at the Bab al-Mandab and offer expanded capacity for an Indian private sector with an increasing demand for data. Additionally, IMEC would advance US national security interests by helping to stabilize the region through expanded economic interdependence, extending the Abraham Accords’ normalization efforts.

Interest in IMEC

The IMEC signatories are at the center of a shifting Eurasian geopolitical scene, in which middle powers are carefully adjusting their alliances and balancing between the US, China, and Russia. The strength of IMEC does not come from its relationship with the current US administration or its role in great power politics but rather from the vested interests of these countries in integrating with each other and advancing their own priorities. For India, that means new international data infrastructure, increased exports, and efficient access to European markets. For Europe, it is about balancing in the new world order and advancing its commercial relationship with India. The Gulf, in turn, is looking to grow into its role as the world’s central logistics hub and developing land routes to export goods that would otherwise be subject to risks or limitations of relying on open access to the Bab al-Mandab and Suez Canal chokepoints. Finally, for the Levant, IMEC would bring investment, jobs, infrastructure, and security through interdependence.

India

India, with its powerful industrial base, stands to gain the most from IMEC. It has shown serious political interest, looking to counter the China-Pakistan Economic Corridor (CPEC), as well as financial interest, with predictions showing that IMEC could lead to an export increase of $22.09bn (5% of total merchandise export value) for India alone.

Indian Prime Minister Narendra Modi’s government has placed enormous emphasis on technology infrastructure expansion, and IMEC’s fiber-optic and energy routes are not just an added benefit to the savings from the route’s efficiency. They are central to IMEC’s appeal. The Indian private sector has a rapidly increasing demand for data as well as the means to invest and build digital infrastructure. India generates nearly 20% of global data but has only around 3% of global data center capacity — closing that gap will require more cross-border data traffic and corresponding investment in the undersea cables that carry it. India’s industrial giants have a history of collaboration with the Gulf in building and running ports, railways, and telecommunications infrastructure both domestically and internationally. For example, DP World and Reliance Industries are partnering to build 700 kilometers of rail in Ahmedabad, and Abu Dhabi’s IHC has invested billions in Adani Group. But right now, technology is foremost in the India-Gulf relationship, and the local semiconductor industry is the priority for India. Fiber-optic cables laid along the corridor provide extreme bandwidth, ultra-low-latency, and high-speed data transmission between Europe, the Gulf, and India at a time when demand is growing rapidly.

“The GCC states are not passive beneficiaries of a Western infrastructure vision. Rather, they are pursuing overlapping bets and building the infrastructure foundations they need, with or without Washington’s backing.”

The Gulf

The Gulf Cooperation Council (GCC) states are not passive beneficiaries of a Western infrastructure vision. Rather, they are pursuing overlapping bets and building the infrastructure foundations they need, with or without Washington’s backing. One example is the UAE’s posture, supporting both IMEC and the alternative Iraq-Turkey Development Road. The UAE is not choosing between competing corridor projects; it is ensuring it has a stake in whichever one prevails. Likewise, GCC grid and rail integration is proceeding at scale regardless of IMEC’s progress, or lack thereof.

The same logic helps explain absences from the IMEC signatory list. Oman’s non-involvement is an interesting omission. Its Duqm Port sits on the Arabian Sea in a position that entirely bypasses the Strait of Hormuz. Routing IMEC’s eastern maritime leg through the strait as opposed to around it looks less like an oversight and more like a miscalculation, especially in light of the US-Israel war with Iran and the resulting closure of the route. Part of the explanation, however, lies in the depth of UAE-India ties — bilateral trade crossed the $100 billion mark in fiscal year 2025, giving Abu Dhabi an advantage in capturing IMEC’s India-facing end. Also, the China-Oman Industrial Park envelops the port and represents approximately $10.7 billion in Chinese investment under a 50-year lease, making it one of BRI’s most significant Arabian projects. Routing a Western-aligned corridor through that port was always going to raise concerns.

GCC grid and rail integration is a funded and contracted program currently under construction and driven entirely by internal economic interests. IMEC’s transport pillar, when it eventually materializes, will land on top of an interconnected GCC infrastructure that is already being built. However, intra-GCC competition has slowed down these efforts. Specifically, there is still a 269-km gap between al-Ghuwaifat in the UAE and Haradh in Saudi Arabia, the cost of laying track for which is estimated at around $2 billion.

Just as oil defined the GCC’s geopolitical weight in the 20th century, its compute infrastructure will define it in the 21st. The corridor and the GCC AI stack share the same spatial logic — both envision the Gulf as connective tissue between India and Europe. IMEC, if it advances, will only accelerate that ambition. And if it continues to stall, the Gulf will seek other frameworks through which to deploy the same capital and achieve broadly the same ends.

Jordan

Jordan has not signed anything official regarding IMEC. That said, the kingdom is crucial to the proposed route because it lies between Saudi Arabia and Israel. Jordan would benefit from investment in rail infrastructure and logistics hubs, and its financial and diplomatic ties with both the UAE and India are notably strong. There have been multiple visits between Jordanian and Indian leaders and investors, including Prime Minister Modi officially traveling to Amman in late 2025. Meanwhile, the Emiratis are Jordan’s largest foreign investors, pouring billions of dollars into infrastructure, real estate, and mining over recent years.

For IMEC to become minimally functional, rail lines need to link the tip of Saudi Arabia’s North-South Railway (al-Hadithah) to the Jezreel Valley railway in Beit She’an, Israel, which connects to the Port of Haifa. The cost to build the line, which would pass through some uneven terrain in northern Jordan, has been estimated at $2.09 billion. Factoring in the cross-border rail and the construction of a rail logistics hub in Mafraq or Amra, that could rise to over $2.5 billion. Given Jordan’s capital constraints and the risk assumed by international investors and lenders dealing with the country, no commitments have been made yet to bridge this gap.

“For IMEC to become minimally functional, rail lines need to link the tip of Saudi Arabia’s North-South Railway (al-Hadithah) to the Jezreel Valley railway in Beit She’an, Israel.”

Israel

Without a resolution to the wars in Gaza and Iran, there is no IMEC. What from the beginning had been its essential precondition — Saudi-Israeli normalization — has become a secondary priority after the more urgent business of containing Iran. For Israel, the corridor is not quite an incentive to normalize or think differently about Palestinian statehood. Israel’s priorities lie elsewhere as it fights what it sees as an existential war on multiple fronts. On the other side of the table, Saudi Arabia remains genuinely open to deeper regional integration, but not to a degree that it will concede its demands for a credible pathway to Palestinian statehood. In addition, public opinion in the kingdom is clear in its opposition to such a move: the Washington Institute in early 2026 found that 99% of Saudi respondents view normalization with Israel negatively. Separately, internal Likud politics have stalled discussions on IMEC rail through Israel.

Current port capacity in Israel is a serious limiting factor for IMEC. Haifa Port, where the corridor is supposed to link the Levant to Europe, represents a key bottleneck as the smallest node on the route by a significant margin, with an annual capacity of roughly 1.5 million twenty-foot equivalents (TEU, the standard, non-physical unit of measurement for cargo capacity in container shipping). A double-stack rail link from Haifa to Ashdod Port (1.5 million TEU/year) could theoretically double total throughput to 3 million TEU. That said, on the opposite side of the Arabian Peninsula, the throughput of Jebel Ali Port in the UAE is over ten times that of Haifa’s. Moreover, the structure of Haifa Port is somewhat complex: its two container terminals are owned and operated separately. Adani Ports, part of the Indian mega-conglomerate Adani Group, owns the legacy Haifa Port (700,000 TEU throughput in 2023) alongside an Israeli firm. The larger, newer terminal, the Bay Port (830,000 TEU), is owned by an Israeli state-owned enterprise but operated by Chinese state-owned Shanghai International Ports Group (SIPG) under a 25-year lease, leaving open potential liabilities for Israeli security and IMEC as a result.

Europe

Europe seeks to reduce its reliance on Chinese trade by increasing its connectivity to the Middle East and India. The EU-India free trade agreement, if finally implemented, is projected to boost bilateral trade by 41% to 65%, a large portion of which could be directed via IMEC. Separately, the 2026 US-Israeli war with Iran has underscored the European continent’s exposure to trade disruptions stemming from the closure of the Strait of Hormuz. An overland railway via the Middle East would provide another outlet for critical goods, such as sulfur and phosphate for fertilizers, to reach their destinations even if shipping in the Persian Gulf — or via the Red Sea — comes under threat.

The corridor’s likely impact on European energy security, on the other hand, could prove less decisive. Despite the EU’s interest in sourcing green hydrogen from the Gulf during IMEC’s conception, that market has yet to develop. And with hydrocarbons, a terrestrial gas pipeline would presumably allow for westward flows from the Gulf — a tempting idea, given the Iran conflict’s severe disruption of global energy markets. But the eagerness on the European side does not center around an IMEC gas pipeline, the return on which was deemed insufficient compared to the $2-4 billion cost of construction. Furthermore, European energy demand is not growing quickly enough, especially in light of the EU’s goals to phase out non-renewable sources over the coming decades. And the EU is looking to do so at a reasonable pace, meeting short- and medium-term hydrocarbon demand with regional sourcing, such as Romania’s Neptun Deep project coming online within a year, which may be able to cover a portion of Eastern Europe’s demand, but, notably, not much more than that.

Structurally, the European end of IMEC is complicated by the same port ownership politics and capacity bottlenecks that define several of the corridor’s Asian nodes. In particular, state-owned China Ocean Shipping Company (COSCO) holds a majority stake in Greece’s Piraeus Port Authority (4.8 million TEU in 2024). The two other candidate European termini are smaller and have also attracted Chineseinterest. The annual capacity of Italy’s port of Trieste is estimated at around 2.7 million TEU, while the French port at Marseille is pegged at approximately 1.45 million TEU.

Marseille carries a separate strategic dimension as one of Europe’s primary subsea fiber-optic cable landing stations. Fiber-optic cables laid along IMEC will crucially connect Europe to the growing numbers of data centers in the Middle East and India.

Parallel Proposals

There are several competing proposals to link the European and Indian markets, but each involves a new set of actors and interests. The routes seek to hedge against geopolitical liabilities and streamline the flow of goods at a time of global uncertainty and instability.

Syria

Tumult in the region has led to increased interest in Syria’s economic vision. After the fall of Bashar al-Assad in December 2024, the Saudis led a push for Syria as a central, more direct route for oil, gas, and telecommunications. Pipelines are moving forward, and the energy sector has backing from major multinational energy companies and $28 billion in contracts. Likewise, Syria’s first international submarine cable will be laid by the Spanish company Medusa. Yet all of these plans assume Syria can fully stabilize and that its infrastructure can be dependably safeguarded from terrorism — a tall order, at least in the short to medium term, for a country exiting 14 years of civil conflict.

Iraq and Turkey

The Iraq-Turkey-Europe Development Road is a multi-billion-dollar project connecting Basra’s Grand Faw Port via 1,200 km of rail and highway through Iraq, into Turkey, and then on to Europe. Qatar and the UAE have pledged to support the project but seem to be waiting for Iraq to try to get it off of the ground first. Abu Dhabi Ports Group will manage al-Faw Port once its construction is completed.

The corridor promises transit that is 10-15 days faster than the Suez route as well as bureaucratic advantages because of Turkey’s EU customs integration. But navigating Iraq’s interior presents a considerable challenge. The security environment is still volatile, and Kurdish and Iran-aligned militias may try to undermine the project. Iran stands to lose a lot if the energy and trade corridor can unhook Baghdad from Iranian energy. Baghdad’s political difficulties with Erbil and its limited bureaucratic and financial power also hamper efforts to make the corridor work. On the Turkish end, despite the links being mostly complete, the rugged terrain, single-tracked and outdated rail, and generally insufficient logistics infrastructure restrict throughput.

With Phase 1 completion targeted for 2028, the corridor would handle 3.5 million TEU. Its final phase will be completed by 2050 and expand the throughput to 25 million TEU. Taken together, the project is comprehensive and provides real competition to IMEC.

Iran and Russia

The International North-South Transport Corridor (INSTC) spans the whole of Iran on land, splits three ways around and through the Caspian, and travels across Russian territory east of Ukraine until landing in Moscow, distributing through Northern Europe. Since 2022, the INSTC has become Moscow’s highest-priority alternative logistics corridor, connecting Russia to Iran, Central Asia, and India, and bypassing Western-controlled infrastructure. A trade corridor on the scale of several hundred thousand TEU could become a powerful tool for furthering Russian interests in Central Asia. Despite the geopolitical complications, the trade route claims to be between 20% and 67% quicker than existing routes, avoiding reliance on the Suez Canal and Bab al-Mandab.

Superficial similarities aside, IMEC and the INSTC fundamentally differ in their purpose, scale, and backers. The INSTC is a rail and fossil fuel corridor designed to help Iran and Russia stay afloat despite their ostracization from global markets, not to connect Indian and European markets in good faith and mutual interest. Second, the INSTC aims to move between 325,000 and 662,000 TEU annually by 2030, making its projected capacity significantly lower than IMEC’s potential 3 million TEU. Third, the INSTC is almost entirely financed from state budgets. Of the $38.2 billion spread across 102 projects, there is very little private capital; instead, the corridor’s build-out is hostage to sovereign budget cycles in Iran, Russia, Kazakhstan, and Turkmenistan. At Iran’s port in Bandar Abbas, cargo splits three ways along thousands of kilometers of rail. For each direction, capacity is severely limited due to trans-shipment costs, rail gauge changes, and outdated or incomplete infrastructure. To the west, a gap between Rasht and Astara raises costs to the point of near economic unviability. In this case, Russia itself is paying for the fix with a €1.3 billion loan to Iran, after President Vladimir Putin’s call for private sector funding received little response. Other problems include the Derbent-Samur chokepoint and snowfalls in the Caucasus, which make a section of the Western route unpassable for 100 days a year.

“IMEC aligned with the Biden administration’s pre-Gaza war push for regional integration efforts in the Middle East.”

US Support

IMEC aligned with the Biden administration’s pre-Gaza war push for regional integration efforts in the Middle East, including through the Abraham Accords and I2U2. The project has transitioned in the second Trump administration to focus more on economic security, supply chain risk, and strategic competition with China. President Trump has publicly championed IMEC, including during a February 2025 joint press conference with India’s Prime Minister Modi. Despite Trump’s skepticism toward multilateral projects inherited from Biden, IMEC roughly fits some of the administration’s priorities by promoting US goals in the region of securing supply chains and pushing back against Chinese influence.

The Trump administration has considered integrating IMEC with the Pax Silica initiative. Led by Under Secretary Jacob Helberg, Pax Silica builds a “coalition of capabilities” for critical minerals, semiconductors, and AI infrastructure, with signatories including India, UAE, Qatar, Israel, and other overlapping IMEC participants. While Pax Silica may align with an advancement of digital infrastructure in these key strategic locations, and while it may “encourage efforts” to partner on digital infrastructure and connectivity, the effort focuses more on domestic mineral refinement and mineral supply chain security than on the goals inherent to IMEC per se.

IMEC does not fit neatly into the Partnership for Global Infrastructure and Investment (PGII) or the Development Finance Corporation (DFC), nor any other major US government funding mechanisms, despite some bipartisan interest. No major binding legislation has passed as of mid-2026. One adjacent effort is the House of Representatives’ Eastern Mediterranean Gateway Act (H.R. 3307), which aims to advance American energy and defense ties with Greece, Cyprus, Israel, and Egypt.

Conclusion

As of May 2026, the implementation of IMEC remains doubtful, with no firm funding commitments or construction timelines put forth. Moreover, the world has changed significantly since the corridor’s original conception. Many of the key relationships that are central to the “New Golden Road” have suffered greatly in this period. Israel’s ties with the Gulf and Jordan have been strained by the wars in Gaza and Iran. Saudi Arabia and the UAE have been heavily — and opposingly — involved in the civil wars in Sudan, Somalia, and Yemen. The Iran war has called the Gulf logistics thesis into question. In this context, sweeping multilateral policy between these states feels much more doubtful than it did when IMEC was announced in Delhi just weeks before the events of October 7, 2023.

Nevertheless, the corridor’s theoretical appeal remains enduring. A more multipolar Eurasia will pursue its interests pragmatically and transactionally — IMEC or not. States understand more than ever their ability to build connectivity in both tech and trade through bilateral partnerships, leveraging the same capital instruments that would fund IMEC. Two and a half years after the initiative was unveiled, the reasons for the corridor’s creation have become more urgent for all parties. Whether it be through IMEC or another competing trans-Middle Eastern transportation project, regional stakeholders are likely to continue working to build out infrastructure that will enable a more interconnected and prosperous future.

This backgrounder was researched and written by MEI spring 2026 intern Walter Murdoch, with input from Senior Fellow Karen E. Young.