In an era defined by the urgent need to combat climate change, the transition to clean renewable energies is imperative to secure the planet's future. Solar and wind power have become important components of this global movement toward sustainability. Yet this transition toward renewable and clean energy sources relies on the availability of critical minerals. Solar power systems, for example, can contain approximately 5.5 tons of copper per megawatt of capacity, mostly in the wiring and cabling needed to transmit electricity from photovoltaic cells. Similarly, with respect to wind energy, onshore wind farms utilize around 3.5 tons of copper per megawatt, while offshore wind installations need as much as 9.5 metric tons per megawatt, mostly for underwater cables.

The role of critical minerals extends beyond supporting solar and wind energy, encompassing a wide range of functions that facilitate emerging technologies and applications for mitigating climate change and decarbonizing the global economy. These functions include advancing low-carbon energy generation, enabling zero-emission transportation, and underpinning digital systems. At the current and projected rate of global population growth, such minerals will have an even more significant role in contributing to economic growth worldwide. This is reinforced by global commitments to achieving net-zero greenhouse gas emissions by 2050 and strategies aimed at fostering growth in advanced manufacturing sectors. Critical minerals are set to be the foundation upon which a sustainable, clean energy future is built, catalyzing innovation and progress on a global scale.

What are critical minerals?

Critical minerals are a group of mineral resources that have paramount importance for the functioning of modern economies and industries, yet their supply is vulnerable to disruption. The designation of "critical" stems from both a mineral's importance to vital technologies and industries as well as risks related to the supply chains. Criticality is dynamic — it changes over time as demand shifts, new discoveries occur, production changes, and geopolitics evolve. A mineral deemed critical today may not be so in the future if alternatives emerge or production expands. Today's critical minerals are primarily rare earth elements and metals that play central roles in advanced technological sectors, such as electric vehicles (EVs), renewable energy, electronics, and defense systems.

The U.S. Energy Act of 2020 highlights the importance of such resources and the U.S. Energy Department defines critical materials as any non-fuel mineral, element, substance, or material that the secretary of energy determines: (1) has a high risk of supply chain disruption; and (2) serves an essential function in one or more energy technologies, including technologies that produce, transmit, store, and conserve energy. Such definitions clearly indicate the significance of these minerals, as well as their dynamic and evolving role, as their availability and accessibility are crucial to technological progress and economic growth.

The list of critical minerals may change based on technological breakthroughs, economic growth, and geopolitical dynamics. The 2023 Critical Materials List, which was published by the U.S. Department of Energy and is similar to the list provided by the International Energy Agency (IEA), includes 50 minerals that are deemed critical. The defined list of critical minerals may differ from country to country based on national and regional priorities. For instance, the lists provided by the European Commission and the U.K. government are not as exhaustive as the list provided by the U.S. Energy Department.

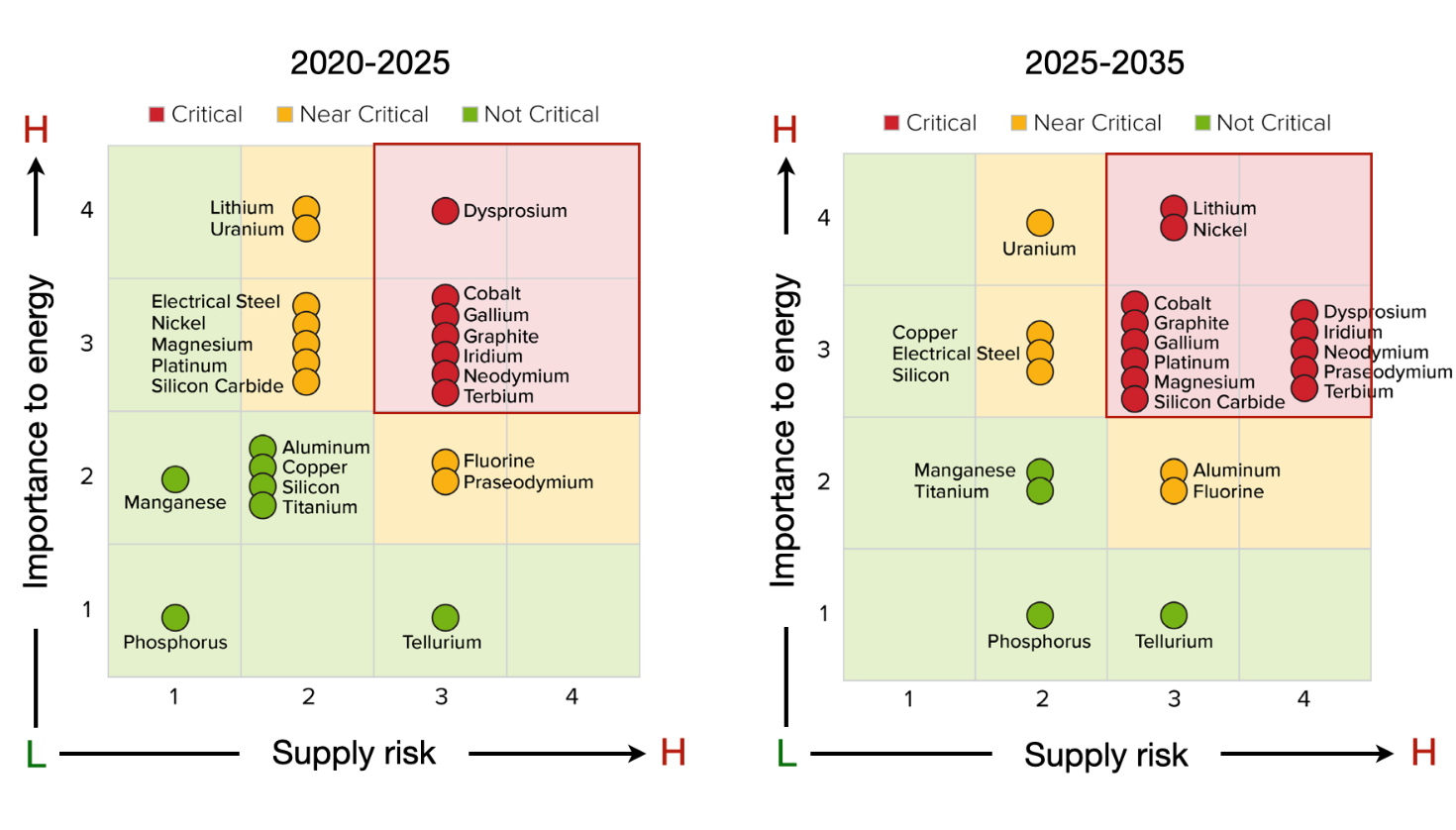

Figure 1 provides a criticality matrix for short-term (2020-2025) and medium-term (2025-2035) outlooks. The criticality of these minerals is affected by the risk to the supply chain and importance to the energy sector, and as we move into the near future, more minerals are shifting from low to high criticality. The growing prominence of critical minerals stems from their indispensable role in technologies vital to sustaining modern life and the global clean energy transition. As renewable energy systems like wind turbines and solar panels proliferate, alongside electronics such as smartphones and EVs, demand for these metals and minerals is surging. However, as the reliance on critical minerals grows, their supply chains are showing increasing vulnerabilities.

Material availability bottlenecks, evidenced during COVID-19, can arise at all process stages from mining to manufacturing. Supply disruptions in minerals like lithium and cobalt could reverberate across the industries that rely on their unique properties, such as batteries and EVs. As the shift to clean energy accelerates, potential constraints securing adequate critical mineral supplies could hamper decarbonization.

Transition to clean energies and role of critical minerals

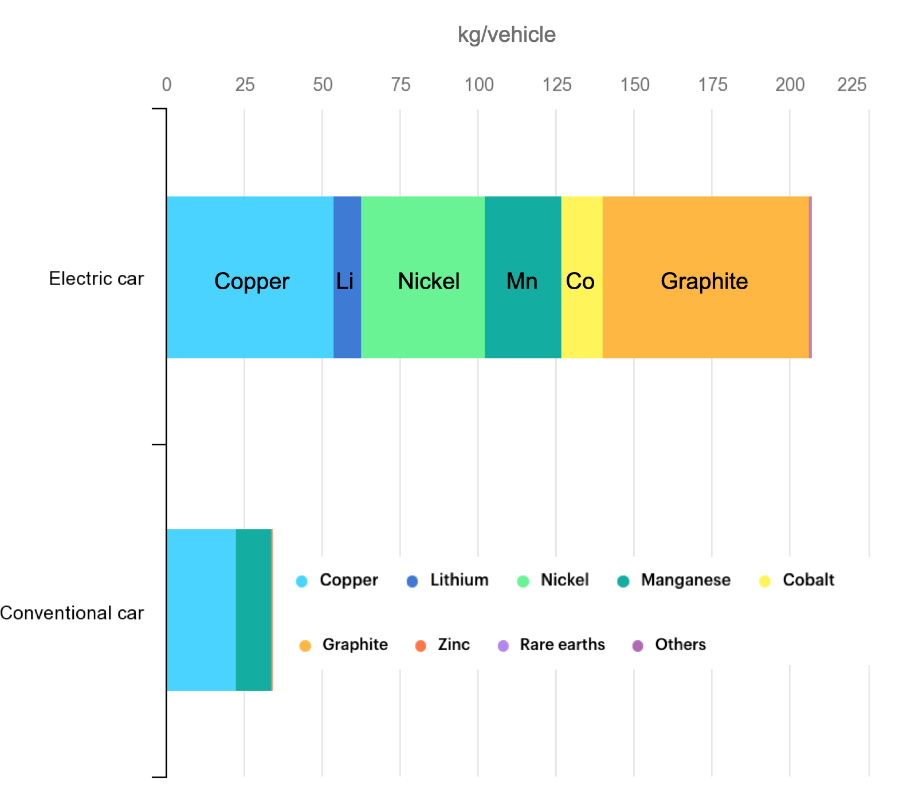

The heightened demand for critical materials also impacts technologies like solar panels, wind turbines, and EVs, which can require several times more minerals than their fossil fuel-based counterparts. For instance, an EV may use six times more minerals than a conventional car, while a wind farm can demand nine times more minerals than a gas power plant per unit of energy capacity. The IEA report on the “Role of Critical Minerals in Clean Energy Transitions” provides context on the existing and expected trends of growth in mineral demands. As countries invest more heavily in clean energy, the average mineral requirements per unit of energy capacity have risen 50% since 2010. Renewables and electrification are becoming the fastest growing aspect of mineral demand.

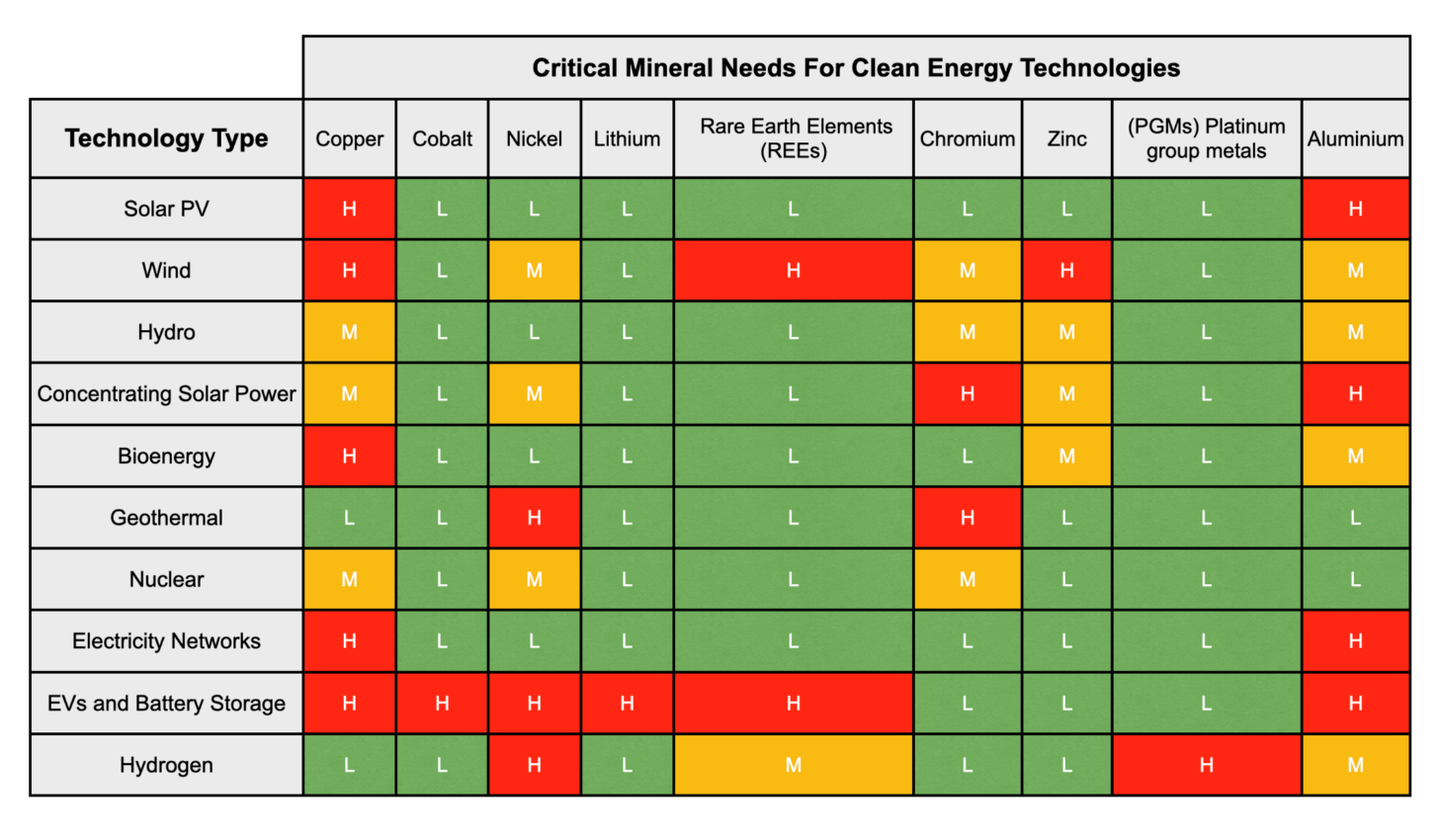

Figure 2 illustrates the variety of critical minerals present in electric cars. Electrifying transportation is considered one of the main ways to mitigate greenhouse gas emissions, but internal combustion engine cars cannot be replaced with EVs without a sustainable supply chain of multiple minerals and metals. Table 1 maps out the critical levels of key minerals for different types of clean energy technologies. The level of criticality of each type of mineral varies based on the clean energy technology they are used for, with corresponding criticality levels of low (L), medium (M) and high (H). A common theme among the different clean energy technologies is that they all require minerals and metals, of which at least two are deemed at a medium or high critical level.

The risks to the mineral supply chain for a clean energy transition could be mitigated by considering a series of parallel approaches. This includes supporting research and development efforts, investing in technology innovation, and improving and reinforcing recycling policies. However, supply reliability cannot be achieved without investing in creating strategic stockpiles for critical minerals, which in turn requires international collaboration and cooperation between producers and consumers. The Middle East has historically been essential in supplying the fossil fuels needed to power the world’s economy, generally acting as a reliable supplier regardless of geopolitical disruptions in the region. As the transition to clean energies and technologies evolve, the region could remain influential and play a key role in ensuring availability of the critical minerals needed for global economic growth and innovation.

The Middle East’s role in securing a sustainable and resilient critical minerals supply chain

Mineral-rich nations are positioning themselves as increasingly influential players in the energy transition movement. For example, the Democratic Republic of the Congo (DRC), home to over 70% of global cobalt reserves, is seeking to derive more value from its minerals and increase local benefits. The DRC recently implemented reforms to its mining code to boost state revenues, and consequently increase its leverage as global cobalt demand surges for EV batteries.

With China currently dominating the processing of lithium, cobalt, and rare earth elements, other nations are seeking to reduce their dependence on a single country for their acquisition of critical minerals. Events like last year’s port congestion in China that disrupted metal exports and Beijing’s imposition of limits on the export of some rare earths have underscored the risks of reliance on limited suppliers. In this context, the resource-rich Middle East is uniquely positioned to provide diversified access to essential minerals, as the region has substantial reserves of minerals that are needed for a clean energy future. Responsible development of the Middle East's mineral wealth, in collaboration with international partners, can enable affordable and reliable global supply chains and support innovation and sustainable growth.

In the Middle East, Saudi Arabia stands out for its critical mineral reserves and bold efforts to develop them through international partnerships. Saudi's western Arabian Shield contains substantial precious metals like gold and silver, plus critical industrial metals such as aluminum, iron, copper, zinc, manganese, and chromium. The Arabian Shield also holds valuable rare earth elements, such as tantalum, for which it has a quarter of the world's reserves and has applications in high-tech industries including electronics, and niobium, which is used in industrial alloys, its applications including jet engines and rockets. The country has recognized the value of these resources in diversifying its economy and generating sustainable revenues in a low-carbon future. The kingdom has prioritized the mining sector in its Vision 2030 economic development plan as a means to reduce its dependence on oil and gas. With over $1.3 trillion in mineral resources, Saudi Arabia aims to catalyze private sector investments in underexplored regions and new environmentally sound extraction approaches.

Already, Saudi mining giant Ma'aden is actively exploring untapped critical mineral reserves. Recently Ma'aden partnered with U.S.-based Ivanhoe Electric to probe Saudi Arabia's relatively under-explored Precambrian Shield for minerals including copper, nickel, cobalt, and lithium. This collaboration exemplifies Riyadh’s intent to develop its strategic minerals in conjunction with allies. Saudi Arabia has also inked an agreement with the U.K. and showed interest in collaboration with mining technology pioneering countries like Australia. A partnership with the U.K. focuses on securing mutual access to vital resources for economic and national security. Meanwhile, a pact with Australia aims to cover collaboration across the entire mineral supply chain, from new exploration to downstream processing. By proactively fostering these international relationships, Saudi Arabia could emerge as a major supplier of the essential resources needed for global decarbonization.

In addition to Saudi Arabia, several other Middle Eastern nations have accelerated efforts to develop their critical mineral resources amid surging demand. For example, Iran recently announced the discovery of significant lithium reserves. Iran’s Ministry of Industries, Mining and Trade, in March 2023, announced the discovery of the first lithium reserve, estimated to be 8.5 million tons of lithium carbonate equivalent, in Hamedan. This discovery, when verified and materialized, positions Iran to potentially become a global supplier of the vital lithium needed in EV batteries and energy storage. It would make the deposit the second-largest known lithium reserve in the world after Chile, which possesses 9.2 million metric tons of the metal. However, attracting the enormous investments required to build extraction and refining infrastructure remains a key obstacle for Iran, given persisting complexities around international sanctions.

Jordan is another Middle Eastern country that is pledging to exploit its mineral wealth to become a major world supplier of vital components for renewable energy systems, such as solar panels and wind turbines. Jordan could carve out an important role in exporting specialized minerals to manufacturing and technology hubs around the world by leveraging its substantial phosphate and rare earth deposits. However, Jordan still needs to overcome hurdles such as bringing on foreign expertise and financing for environmentally and socially responsible mining.

Turkey is also advancing plans to develop its critical mineral reserves, with a focus on rare earth elements that are needed in advanced magnets and batteries. However, uncertainties about concentrations of rare earths in Turkish mineral deposits pose technical challenges for viable extraction. Attracting international partners with advanced separation capabilities could enable Turkey to harness its resources.

However, it’s worth noting that while lithium has seen surging demand as a key component of EV batteries, some major automakers like Ford have recently scaled back plans for large battery plants in certain regions. Factors like softening EV sales, rising materials costs, and localized policy incentives have led certain companies to downsize or postpone billion-dollar battery factory builds. Nevertheless, the long-term trajectory still points to massive lithium battery investments globally to support electric mobility growth toward 2030 and beyond. Near-term pullbacks by select automakers do not negate the overall enormous project pipeline that requires reliable lithium supply chains. But it does underscore the complexity of scaling up nascent battery technologies and manufacturing capacities in alignment with evolving demand.

The Middle East has clear advantages when it comes to potentially supplying critical minerals that are essential for global decarbonization. The region has a wealth of untapped resources, which reduces the need for new extractive capacity that often faces strong societal opposition. Existing capabilities in mining, processing, and logistics that were developed for fossil fuels can be leveraged for critical resources. However, there are still obstacles to fully capitalizing on the Middle East's mineral resources. Attracting substantial international investments requires competitive fiscal terms and predictable regulations to incentivize the participation of private companies. Additionally, strict environmental and social safeguards need to be implemented to ensure ethical and sustainable mining, and enhancing energy efficiency will be critical for the energy-intensive processes involved in refining minerals and metals.

Nations like Saudi Arabia, which have access to technology and financing, may progress rapidly in overcoming these hurdles. However, other emerging producers in the region face steeper challenges in developing their mineral cache independently. Working with international partners is key, but complex regional geopolitics can complicate matters. For example, Iran faces unique challenges due to limited access to technology, investment, and partnerships. Despite this, Iran's resource-rich landscape, including critical minerals, makes it an attractive prospect, particularly for partners that can provide the necessary support to cultivate these minerals, such as China. This is well aligned with China's active efforts to secure critical minerals. Its involvement in political and economically unstable Afghanistan, which has vast strategic mineral resources, underscores its focus on maintaining a robust critical minerals supply chain. Concerns persist over China's growing influence and the need for diversified partnerships.

However, the region's collective mineral abundance can still help reduce its dependence on any single dominant supplier like China. Diversified sourcing is crucial for technology companies and nations to mitigate their supply risk. From this perspective, a greater global role for Middle Eastern mineral producers enhances resilience against potential shocks, which is why many major world economies are proactively expanding ties with the region. The U.K.'s new Critical Minerals Intelligence Centre reflects the growing global recognition of these resources' immense strategic value and the need to secure sustainable supplies. Critical minerals are moving beyond niche materials to occupying a center stage in geopolitical and economic competition. Their essential role in technology and energy security makes access to them a priority for governments worldwide.

Conclusion

The Middle East holds promising potential as a major supplier of the critical minerals and metals essential for the global transition to clean energy. As demand surges for the elements inside batteries, solar panels, and wind turbines, the region's mineral resources will become a strategic priority. Responsible development of these resources, in collaborative partnership with allies, allows the Middle East to continue advancing climate resilience.

While obstacles like attracting investment and technology integration remain, signs already point to the region's growing awareness around its mineral wealth and exploring ways to leverage it. Saudi Arabia and others recognize the immense value of their minerals in diversifying economies and powering the world's low-carbon future. By leveraging its resources wisely and adhering to high standards, the Middle East can help forge more secure and sustainable mineral supply chains worldwide. This can enable the innovations that drive equitable growth and prosperity in a decarbonizing world and propel the Middle East's mineral-rich nations to the forefront of climate mitigation.

Hamid Pouran is the program leader for MSc Sustainability and Climate Change at the University of Wolverhampton.

Photo by Tasneem Alsultan/Bloomberg via Getty Images

The Middle East Institute (MEI) is an independent, non-partisan, non-for-profit, educational organization. It does not engage in advocacy and its scholars’ opinions are their own. MEI welcomes financial donations, but retains sole editorial control over its work and its publications reflect only the authors’ views. For a listing of MEI donors, please click here.