Originally posted January 2008

"In the past week Iran’s president, Mahmud Ahmadinejad, has damned it as a ‘worthless piece of paper’ and China’s premier, Wen Jiabao, has moaned that it is causing his country ‘big pressure’. The dollar’s relentless decline—it hit a new low of $1.49 against the euro on November 21st—is prompting jibes from America’s critics, jangling investors’ nerves and giving policymakers headaches."[1]

"Currency systems are like marriage: whichever one you find yourself in you think another one might be better."[2]

Introduction

Throughout most of 2007, hardly a week went by without a new reason to be concerned about the fate of the US dollar. Toward the latter part of the year, the distressing news broke that key members of the Gulf Cooperation Council (GCC), the UAE and Qatar in particular, might abandon linking their currencies with the dollar. Such an event would reduce the overall demand for the dollar and place even more downward pressure on it. Many experts believed that the GCC’s delinking from the besieged currency might even precipitate a mass exodus to the euro or even the Chinese yuan.

With the exception of Kuwait, which switched to a currency basket in May of 2007, all Gulf Cooperation Council (GCC) countries maintain dollar pegs. The reason for the dollar peg is straightforward. The United States is one of the GCC’s biggest trading partners. Crude oil is traded globally in dollars. GCC governments earn and spend in dollars. Most of the estimated 41.5 trillion public sector assets in the Gulf are dollar-denominated, and the booming project market is backed by dollar lending.

Pegging local GCC currencies to the dollar has been a long-standing practice. Saudi Arabia and the UAE, for example, have had USD pegs since June 1986 and January 1978, respectively, and, for the most part, dollar pegs have worked well for them as the sole nominal anchor for inflation control. Similarly, before July 2005, China had a de facto dollar peg for 11 years (since January 1994), for exactly the same reason.[3] However, with the prolonged fall in the dollar since early 2000, the picture has changed dramatically. On average, GCC member countries’ currencies have declined on average 30-40% against the euro, making non-dollar imports significantly more expensive. In the three years ending December 2005, the International Monetary Fund (IMF) estimates that the real value of the Saudi riyal fell by about 18%, even as the real price of oil nearly tripled.[4]

For the region as a whole, the effect has been to reduce individual purchasing power significantly, since dollar denominated goods from the United States account for only about 10% of both GCC exports and imports.[5] The pegged exchange rate and falling value of the dollar have also been cited as one of the causes of increased labor unrest, especially in Dubai where many foreign workers are being impoverished by the combination of rising local prices and the falling dollar. As one account described the situation in late 2007:

Usually, migrant laborers in the UAE are paid in dirhams, the local currency that is pegged to the dollar. As the value of the dollar falls, workers grow increasingly desperate as the buying power of their wages dwindles. As inflation in the UAE creeps towards 10 per cent, the workers’ hopes of saving money are dashed. Without a pay rise, the workers say that they can no longer afford to support relatives back home — the reason that overwhelmingly draws them here in the first place. The jobs that once seemed lucrative now feel like a waste of time, they say. Many believe that they would be better off to cut their losses and return to India or Pakistan, where the local currency is looking increasingly attractive.[6]

The rumors of a change in GCC exchange rate policies began in May 2007, when Kuwait shifted its peg with the dollar to one of a basket of currencies (with the dollar still accounting for 70-80% of the value). Although the shift amounted to only a 1% revaluation, Kuwait’s action ignited speculation that several or all of the other GCC countries might either revalue or delink their currencies from the dollar.[7]

The currency issue came to a head when the heads of state of the Gulf Cooperation Council met in Doha, Qatar on December 3, 2007 to discuss whether or not to alter their existing dollar pegs. According to a report entitled Gulf Currencies, Change Needed and Likely, written before the meeting by Gerard Lyons and Marios Maratheftis at Standard Chartered: “A revaluation of the GCC currencies is needed now and the region should begin preparations to shift their currencies away from a peg to the dollar to managing their currencies against a basket of currencies with which the Gulf trades.”[8]

Lyons and Maratheftis went on to suggest that: “This shift in currency pegs is needed not only to reflect the present vulnerable state of the dollar, but more importantly to help position the region’s economy for both the cyclical and structural shifts that it is undergoing.” In the past, the GCC’s dollar peg has brought benefits. “The decision to peg their currencies to the dollar achieved credibility by tying the region’s monetary policy to that of the US Fed, and also achieved certainty in the minds of the general public. There is, however, a cyclical challenge,” Lyons and Maratheftis add:

As the UK found to its cost when it was tied to Germany and the Deutsche Mark in Europe’s Exchange Rate Mechanism in the early 1990s, once there is a disconnect between the policies needed at the center of the system and those needed elsewhere then problems develop. A similar episode, albeit different in scale is now being seen in the Gulf. Whilst the US is cutting interest rates in response to a slowing economy the Gulf needs a tighter monetary policy to curb inflation. And, even though the Gulf is deepening and developing its capital markets, it does not yet have sophisticated enough capital markets to sterilize or neutralize the local build up of liquidity – which of course continues as the region booms and oil prices stay high.[9]

Despite such calls for action, the December 3-4 Gulf Summit ended without any change in the dollar peg. Asked whether GCC member states would de-peg their currencies on their own, Saudi Arabia’s Finance Minister Ibrahim Al Assaf told reporters that if the countries did it they would do it as a block. However, conflicting information from many GCC leaders is fanning the flames of speculation. Recent announcements from the United Arab Emirates (UAE) and Qatar have indicated their wish to abandon the dollar. Yet statements made during the leaders’ summit have leaned towards keeping the currency pegged until the group’s monetary union is formed in 2010.

Still, the exchange rate issue remains and is unlikely to go away anytime soon. Is it time, as suggested above, for the GCC countries to seriously consider breaking their currency pegs with the dollar? To shed some light on this important issue, the sections below outline the main issues surrounding the current currency debates. First, how does the current pegged system work? Second, what is the rationale for maintaining the existing system, at least in the near term? Third, what are the main costs in maintaining the status quo? Fourth, which of the alternatives above appear best suited to the member country’s needs at this point in time? Finally, with these considerations in mind, what might we expect the GCC countries to do with regard to their exchange rates over the next several years?

Workings of the Dollar Peg System

The most often cited advantage of pegging to the dollar is that it allows an emerging economy — especially one with weak economic and political institutions — to quickly build confidence in its currency by adopting the relatively inflation-free monetary policy of the United States.[10]

The operational workings of the peg are fairly straightforward[11] — to support the peg, all a country needs to do is have enough foreign currency to be able to buy and sell its currency at the fixed exchange rate. Using Saudi Arabia as an example, to support the peg the central bank (SAMA) holds by law sufficient “foreign exchange convertible to gold” (principally short-term US dollar instruments) to cover the value of all printed riyals in circulation, the part of money supply known as “MO.” In fact, today SAMA holds foreign currency-denominated assets far in excess of that required to provide 100% coverage of the currency.[12]

Advocates of the peg note that it has served its purpose in providing stability. In terms of internal stability, inflation in Saudi Arabia averaged a negligible 0.5% per annum between 1986 and 2006. External stability is measured by the “real effective exchange rate,” which takes into account the value of the riyal against the currencies of Saudi Arabia’s main trade partners. According to the IMF, the real effective exchange rate has been relatively stable apart from periods of significant dollar weakness in 1986-1987 and 2002-2005.

While the overall record of the Saudi riyal’s peg to the dollar has been excellent, problems have occurred:

Oil market developments have occasionally led to pressure on the peg. In 1993 falling oil prices, combined with concerns about the budget and current accounts deficits, generated money market speculation that the riyal would be devalued. Similar speculation occurred during late 1998 and early 1999 owing to a combination of falling oil prices and an economic crisis in Asia that caused major exchange rate devaluations in that region. At that time, SAMA successfully intervened in the foreign exchange markets with its vast foreign asset position to maintain the stability of the riyal.[13]

The Case for Maintaining the Peg

No doubt the Saudi position at the December 2007 Council of Ministers meeting was the decisive factor in the GCC’s decision not to alter the exchange rate system at that time. As for the future, Saudi Arabia will likely remain the biggest advocate of maintaining the pegged exchange rate:[14]

- Saudi Arabia is not only generally the most conservative state in the GCC, but also the most deeply invested in its security partnership with Washington.

- The Saudi commitment to dollar-based oil wealth recycling goes back to high-level bilateral agreements in the 1970s, which ushered in a period of unprecedented technical and economic cooperation.

- As a relatively populous state with large fiscal commitments, the kingdom has a specific interest in keeping the value of its overseas reserves as high as possible.

- A riyal appreciation would decrease the value of its assets, which have been estimated to be 75% dollar-denominated.

- A Saudi movement away from the dollar could trigger a panic, which could further undermine both the value of overseas assets and the global economic system.

In addition, many economists in Saudi Arabia emphasize the high costs associated with either abandoning the peg altogether or letting the currency revalue in a managed float. The losers in such action are easily identified:[15]

The government: Oil revenues are earned in dollars and converted into riyals for budgetary spending. A revaluation would permanently impair the riyal value of oil revenues, reducing the size of the current budget surplus and accelerating the day when the budget falls into deficit. The value of the government’s mostly dollar-denominated foreign assets, currently in excess of $240 billion when converted into riyals, would also be reduced considerably with a significant revaluation.

The Central Bank (SAMA): SAMA has stated repeatedly and forcefully that there would be no change to the 21-year-old exchange rate peg. Any move would, therefore, damage SAMA’s credibility and reduce confidence in the currency in the event of an oil price downturn or increase in the value of the dollar. Moreover, no central bank wants a sudden and sharp adjustment to the exchange rate, but small changes would have little impact on those hit by dollar weakness.

Foreign investors: A more expensive riyal and the introduction of exchange rate uncertainty would discourage foreign investment, thus reducing much needed technology transfer. As the government is considering opening its capital market to foreign investors, a revaluation would make that more costly.

Local companies: Revaluation of the riyal would undermine Saudi efforts at diversification away from oil — the “Dutch Disease” effect.[16] Saudi companies that currently export or hope to export in the near future would see their products become more expensive overseas, making them less competitive. Those whose goods compete with imports, such as many food products, building materials, and furniture, would suffer as imported products became cheaper.

There are several additional arguments against a revaluation of the Saudi riyal:[17]

- Inflation would not be completely addressed. Price rises in the kingdom are mainly domestically generated. Imported inflation accounts for about 35% of total inflation. A large part of this is food-related, which is a global phenomenon, not just a Saudi one. A revaluation will not necessarily help reduce these costs to consumers.

- Today’s revaluation could be tomorrow’s devaluation, which would make the kingdom’s currency regime less credible. International investors might view this currency uncertainty unfavorably as they assess risks.

- One revaluation could lead to subsequent ones, which could eventually put the peg into question.

In sum, the Saudis, as well as advocates of the dollar peg in other GCC countries, stress the fact that costs associated with a revaluation are likely to be considerable. Peg advocates implicitly assume that any possible benefits associated with improved macroeconomic stabilization and increased purchasing power for average Saudis are likely to be relatively low. Perhaps in the future, as the economy becomes more diversified, domestic financial markets deepen, and the central bank develops viable monetary policy instruments, a more flexible exchange rate might make sense. However, that time has not arrived, and changing the exchange rate prematurely would do more harm than good.

Constraints Imposed by the Peg

While there is little doubt the pegged exchange rate system has served Saudi Arabia and the other GCC countries well in the past, critics are quick to point out that pegs come at a high cost — specifically, the loss of an independent monetary policy. Economic theory postulates that targeting an exchange rate and maintaining an independent monetary policy with an open capital account to be an “impossible trinity” (i.e., two of these three objectives can be achieved, but not all three at the same time).[18]

It follows that countries pegged to the US dollar must follow the monetary policies in that country. If they have business cycles that are in sync with that of the US, the appropriate monetary policies in these countries should be similar to those of the US, and changes in the Fed’s policy should not really cause complications. However, if these countries diverge from the US economy’s business cycle, as is currently the case, then monetary policy that is good for the US will not be appropriate for these countries.

The necessity of similar monetary policies in the GCC to those in the United States under the peg stems from the fact that to maintain a pegged exchange rate GCC central banks are forced to follow the interest rate moves of the US Federal Reserve. Any significant deviation in rates would lead to arbitrage by currency traders placing strain on the peg and possibly inviting destabilizing speculation, such as occurred in 1997 with the collapse of the Thai baht.

The relevant question for the GCC countries is at what point the advantages of the stability and certainty of the peg are less than the costs associated with their inability to stabilize the domestic economy through pursuing an independent monetary policy. For years, the issue was somewhat moot because the GCC countries did not have either the monetary expertise or the financial market sophistication necessary to pursue an independent monetary policy. This may no longer the case.

Problems in Responding to Inflationary Pressures

Currently the US is lowering interest rates to stave off a recession. The appropriate policy for combating inflation in the GCC is higher interest rates.

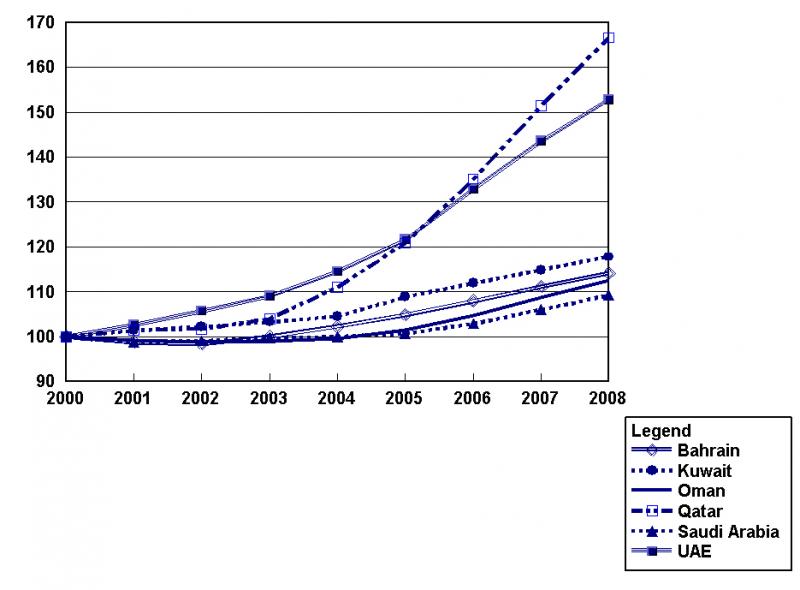

The GCC members’ difficulty in combating inflation is compounded by the weakening of their currencies as the dollar depreciates in international currency markets. The effect is to amplify the inflationary effects stemming from the increase in world food prices. Much of the pressure is from rising world food prices, which are a bulky item in consumer price indices.[19] Clearly, the inflationary impact of rising international food prices combined with a depreciating dollar will vary from country to country depending on the composition of its imports. Similarly, varying fiscal rates of expansion, together with structural differences have created several unique patterns of inflation among the GCC countries (Figure 1 and Table 1):

- Low inflation group with relatively low single digit inflation: Saudi Arabia, Kuwait, Oman and Bahrain where the inflation rates in recent years have been in the 2-3% range.

- High inflation group: Qatari and UAE rates have reached 9-12%. Given that these rates are considerably above that of the other group, excessive domestic demand is likely to have played a significant role in accelerating the recent price increases.

Table 1: Inflation in the GCC Countries, 2000-2008 (Average Annual Rates of Growth)

|

Country |

2000 |

2001 |

2002 |

2003 |

2004 |

2005 |

2006 |

2007 |

2008 |

|---|---|---|---|---|---|---|---|---|---|

|

Bahrain |

-0.7 |

-1.2 |

-0.5 |

1.7 |

2.3 |

2.6 |

2.9 |

2.9 |

2.7 |

|

Kuwait |

1.6 |

1.4 |

0.8 |

1.0 |

1.3 |

4.1 |

2.8 |

2.6 |

2.6 |

|

Oman |

-1.2 |

-0.8 |

-0.3 |

0.2 |

0.7 |

1.9 |

3.2 |

3.8 |

3.5 |

|

Qatar |

1.7 |

1.4 |

0.2 |

2.3 |

6.8 |

8.8 |

11.8 |

12.0 |

10.0 |

|

Saudi Arabia |

-1.1 |

-1.1 |

0.2 |

0.6 |

0.4 |

0.7 |

2.2 |

3.0 |

3.0 |

|

UAE |

1.4 |

2.7 |

2.9 |

3.2 |

5.0 |

6.2 |

9.3 |

8.0 |

6.4 |

It should be noted at this point that although all of the GCC consumer price indices show a clear upward trend over the last several years, measurement errors in official price indices are likely to underestimate inflation throughout the GCC. For example, Morgan-Stanley[20] cites independent surveys suggesting an inflation rate of 15-25% in the UAE as opposed to the much lower official figures. “Given the extent of liquidity abundance and the mix of extremely accommodative macroeconomic policies, the behavior of non-tradable prices is the obvious culprit. But we should not overlook the role of imported inflation. Pegged to the dollar, the currencies of oil producers in the Middle East have tracked the dollar’s sustained depreciation since 2002, even as their export earnings have soared to record levels. And since the majority of imports come from Europe and Asia, the dollar’s weakness has become a major source of inflation by pushing up the price of imported goods and services.”[21]

While higher import prices have contributed to increases in inflation in recent years, varying inflation rates between the two groups of GCC economies largely reflect differences in the pace of increase in public spending and investment. As noted above, inflation was strongest in Qatar and the UAE, where population growth has outpaced the provision of accommodation resulting in a sharp increase in rents. Rental increases account for half of inflation in the UAE, overwhelming the mitigating effect of importing low-wage labor.[22]

For the UAE and Qatar, the normally prescribed policies of tighter monetary policy and higher interest rates to fight inflation would only lead to massive inflows to take advantage of the higher interest rates — the surge in demand for local GCC currencies would put upward pressure on the exchange rate that could conceivably collapse the peg. In short, under the current exchange rate system, the UAE and Qatar are precluded from tightening monetary policy — normally an effective tool in combating inflationary pressures.

The example[23] of Qatar is especially instructive. Currently the country is caught in a catch-22 in that it cannot reduce interest rates at the same pace as the US Federal Reserve due to high local liquidity and inflation. This situation is leading to a widening differential between US and Qatari interest rates and stimulating the inflow of increased liquidity. The resulting options would be to restrain liquidity by possibly raising bank-required reserve ratios, but these can only go so high. The other option is raising interest rates, which would only further speculation about de-pegging the riyal, again attracting a large inflow of funds hoping to benefit from a pending revaluation.

As Qatar continues to see a steady rise in inflation, there will be increasing pressure to de-peg the currency. The biggest question will remain whether to keep the dollar peg and weather the current storm until the monetary union is formed or to make a move now to ease pressures until a monetary union is in place.[24]

Difficulties in Preventing Destabilizing Speculative Capital Flows

As noted above, even without interest, efforts to arbitrage the pegs are currently under considerable pressure due to speculative flows. While these flows have become a major worry of central bankers all over the Gulf, they are most pronounced in Qatar and the UAE. The problem came to a head in late 2007, when GCC governments did not immediately follow US interest rate decreases in September. Speculators saw this as a sign of an impending revaluation of their currencies.

Other signs that further fueled speculator’s expectations of revaluation included:

- A Qatari statement that the country's sovereign wealth fund had reduced its dollar exposure by more than half to around 40%;

- Increasing calls, including one from the IMF, for revaluation and/or adoption of a currency basket instead of a dollar-only peg;

- GCC states' agreement in September that, notwithstanding their plans for monetary union by 2010, they would be allowed to pursue separate inflation policies; and

- Remarks by the head of the UAE central bank about the possible need for a revaluation and for tying the dirham to a currency basket.

Against this background, currency traders bet on a revaluation of GCC currencies. Although several central banks decreased interest rates in November to conform to the US Federal Reserve moves, there was a widespread expectation that the GCC summit would pave the way for devaluation and a quick profit for the speculators. Instead, as noted above, it produced no statement at all on the issue. Clearly, as long as the pegs stay in place, speculative movements will flare up from time to time, making it even more difficult for central banks to control liquidity and ultimately the rate of domestic inflation.

Advantages of More Flexible Exchange Rates in the GCC Region

The main arguments against retaining pegged rates tend to be more theoretical than those stressing the status quo. Advocates of more exchange rate flexibility usually stress the role of exchange rates in absorbing shocks and relieving stress on the domestic economy. For example, Brad Setser[25] contends that oil-exporting economies that now peg to the dollar would be better served by a currency regime that assures their currencies depreciate when the price of oil falls and appreciate when the price of oil rises — a pattern likely to exist during most times under a regime of floating exchange rates. He notes that those that are unprepared for a managed float should peg to a broader basket that includes the price of oil.

The logic for breaking the peg and adopting a more flexible exchange rate regime draws on the economic theory of shocks and balance of payments adjustment. Classic economic analysis differentiates between temporary and permanent shocks to the price of oil, as well as between supply and demand shocks. A temporary shock does not require adjustment. An oil-exporting economy should save the oil windfall rather than permanently increasing consumption and investment, while the oil-importing economy should dip into its savings to cover a temporary rise in the price of oil rather than cutting back on its consumption and investment.

On the other hand, a permanent rise in the price of oil, by contrast, allows higher levels of levels of consumption and investment in the oil-exporting economy and necessitates a lower level of consumption and investment in the oil-importing economy. A permanent shock should lead to strong economic expansion in oil-exporting economies and real appreciation of their currencies, while having the opposite effect on oil-importing economies. The movements in currency values would assist the restoration of balance of payments equilibrium while the appreciating currencies of the oil exporters would help suppress the inflationary impacts of increased domestic expenditures.

In contrast to a system of flexible rates, the dollar peg is likely to produce an excessive amount of deflation or inflation as economies adjust from shocks since all the pressure for adjustment is placed on the domestic economy. As a specific example, an increase in the price of oil implies a temporary rise in inflation; a fall in the price of oil implies a period of deflation. Setser describes the process as follows:

Holding the nominal exchange rate constant and allowing all the real adjustment to come from changes in the price level has two important consequences. First the process of inflationary and/or deflationary adjustment is slow. Much of the rise in domestic prices associated with a rise in the oil price will come after the price of oil has stabilized. Moreover, once started, inflationary adjustment can develop its own momentum as economic agents anticipate rising price levels and demand higher nominal wages. In some cases the resulting inflationary momentum pushed up the real exchange rate even after oil prices had turned down, setting the stage for a real overvaluation.[26]

A typical scenario with fixed exchange rates begins with an increase in the price of oil. In turn, this leads to an increase in government revenue, spending, investment, and inflation. Because interest rates tend to adjust slowly, high inflation tends to result in negative real interest rates (the nominal interest rate minus the rate of inflation). Fiscal and monetary policies turn expansionary at the same time. Negative real rates fuel a surge in speculative property investment. They potentially set the stage for a boom/bust cycle driven by an unsustainable surge in private investment, land speculation, and an asset market bubble. The same dynamics also work in reverse: a fall in the oil price leads to a fall in revenue, a fall in spending, inflation, if not deflation and a rise in real interest rates.

In short, the sophisticated case against pegged exchange rates is that they contribute to highly pro-cyclical macroeconomic policies — inflations are likely to be higher and recessions more severe than would likely be the case under a system of flexible exchange rates.

Assessing the Options

The GCC countries have experienced three rather distinct shocks in recent years: (a) a positive oil price shock; (b) the anchor currency — the US dollar being in a protracted and sharp descent; and (c) the US Federal Reserve’s policy being out of sync with the GCC’s needs. Among the several alternative regimes that have been mentioned in the previous sections, logical variants include:

- A small revaluation of perhaps 3-5%, which could be the first of several steps of adjustment;

- A large revaluation of 20-30% that could take all speculative pressure of the currencies at once, as generally advocated by international economists; and

- The adoption of a currency basket in which the dollar would initially be given a dominant weight that could be progressively reduced.

- The adoption of flexible exchange rates.

The first two options, while possible, would not, as noted above, enable the countries to avoid many of the problems associated with the fixed peg currency. They might even create a more unstable situation of volatile capital inflows if speculators interpret the changes as signals that future revaluations were soon to be in the works.

Clearly, an abandonment of the dollar peg has geopolitical as well as economic ramifications. Shifts towards a looser peg by the GCC countries would contract the so- called “dollar zone” — an area where countries settle their international transactions and payments using the dollar. Currently, the de facto dollar zone includes China, Japan, and many of the East Asian countries, as well as the oil-exporting members of the GCC — in essence the two main blocs of balance-of-payments surplus.[27] Clearly, a shift of this magnitude in the international system would have a negative impact on the value of the dollar. At best there would simply be a lower demand for dollars; at worst, there might be a stampede away from the dollar, resulting in a sudden and dramatic fall in its value. Reportedly, this possibility is a major factor behind Saudi Arabia’s reluctance to abandon the dollar peg.[28]

The third option, a currency basket perhaps along the lines of the one adopted by Kuwait in 2007, has its pros and cons. It would help stabilize exchange rates but could still leave individual currencies divorced from price movements in oil markets. A variant might be to go to a mixed commodity basket that includes the export price of crude. However, with the establishment of a currency union only several years away, member countries might feel that to be the appropriate time to review and consider the advantages of such a major policy shift.

A managed free float always looks good in theory and on paper. As noted above, it has the advantages of relieving the domestic economy of some of the adjustments following shocks, but there is the operational issue of whether the GCC countries have the institutional framework to effectively implement this type of regime. As Jen and St-Arnaud note:

The best exchange rate regime for the GCC countries, in theory, is a managed float, in our opinion. However the main reason why the GCC are still contemplating various forms of pegs is the relatively ineffective monetary instruments that render an independent monetary policy a non-viable option at this point. This practical concern brings the GCC countries to square one of the debate: if the GCC need a peg of some form, a dollar peg is arguably no worse than other pegs. This is why there are still some members of the GCC for maintaining the dollar peg, as an interim regime.[29]

In any case, there are no signals suggesting that the GCC countries feel their monetary institutions and financial markets are at the point where the introduction of a flexible exchange rate regime would be a distinct improvement over the status quo.

Clearly, a factor to consider in any future exchange rate systems is their ability to facilitate the formation of the currency union, tentatively scheduled for 2010. In addition, the exchange rate regimes in place before that date will no doubt dictate the nature of the new common currency.

In this regard, the countries have agreed to five criteria for a European Union-style economic union, including capping budgets at 3% of gross domestic product, capping public debt at 60% of GDP and inflation at the GCC average plus 2%. Interest rates are to be no higher than the average of the lowest three states plus 2% and countries must have foreign exchange reserves to cover four to six months of imports. As things stand, the existing dollar pegs may be the best system to meet these criteria.

Future trends in inflation and the value of the dollar are also prime considerations. By the time a Gulf monetary authority is in a position to review the dollar peg, the urge to drop it may be far less pressing. While inflation is a concern now, this may not be the case in 2010. For one thing, the current wave of major expenditures will have passed, allowing supply bottlenecks to be alleviated. Countries like the UAE are targeting the rental market for major expansions to relieve the inflationary pressures in that segment of the economy. This should produce a significant drop in that country’s inflation.[30]

While the future value of the dollar is just about impossible to predict, one thing is certain — it will not continue its downward slide indefinitely. For one thing, this would set off a major recession in the EU as that region’s products are priced out of international markets. This effect would be reinforced if China retains its quasi peg to the dollar. There is also a certain resiliency in the dollar that is often overlooked[31] — clearly if the dollar were to stabilize or regain some of its lost value, there would be even fewer reasons to abandon the peg.

Perhaps Lidstone sums it up best: “There are big advantages to being pegged, after all. For a start you don’t have to do anything (in terms of monetary policy). And you can take advantage of hedging instruments and other aspects of dollar markets the world over. In the end it may prove easier for the GCC states to stick with the devil they know.”[32]

[1]. “The Dollar: Time to Break Free,” The Economist, November 22, 2007, http://www.economist.com/opinion/displaystory.cfm?story_id=10177927.

[2]. George Soros, quoted in Peter Wilson and Henry Ng Shang Ren, “The Choice of Exchange Rate Regime and the Volatility of Exchange Rates after the Asian Crisis: A Counterfactual Analysis,” The World Economy, Vol. 30, No. 11, November 2007, p. 1646.

[3]. Stephen Jen, “Dollar Peggers to Stretch the ‘Impossible Trinity,’” Morgan Stanley Global Economic Forum, September 28, 2007, http://www.morganstanley.com/views/gef/archive/2007/20070928-Fri.html.

[4]. Digby Lidstone, “Fixed Ideas,” Middle East Economic Digest, Vol. 50, No. 39, September 29, 2006, pp. 4-5.

[5]. “Gulf States: Conflict Over Currency Revaluation Frozen,” Oxford Analytica, December 7, 2007

[6]. Sonia Verma, “Dark Side of Dubai’s Economic Boom Exacts Harsh Human Toll,” London Times, November 3, 2007, http://business.timesonline.co.uk/tol/business/markets/the_gulf/article….

[7]. Lidstone, “Fixed Ideas,” pp. 4-5.

[8]. Gerard Lyons and Marios Maratheftis, Gulf Currencies: Change Needed and Likely (London: Standard Chartered, November 15, 2007), http://www.standardchartered.com/media-centre/press-releases/2007/docum….

[9]. Lyons and Maratheftis, Gulf Currencies, pp. 1-2.

[10]. Brad Setser, “The Case for Exchange Rate Flexibility in Oil-Exporting Economies” (Washington: Peterson Institute for International Economics, August 2007), Policy Brief PB07-8, p. 1, http://www.iie.com/publications/pb/pb07-8.pdf.

[11]. The following draws on Brad Bourland, The Riyal’s Peg to the Dollar (Riyadh: Jadwa Investment, August 2007).

[12]. Bourland, The Riyal’s Peg to the Dollar, p. 2.

[13]. Bourland, The Riyal’s Peg to the Dollar, p. 3.

[14]. “Gulf States: Conflict Over Currency Revaluation Frozen,” Oxford Analytica, December 7, 2007

[15]. Bourland, The Riyal’s Peg to the Dollar, Part 1.

[16]. Serhan Cevik, “A Dutch Disease in Arabia,” Morgan Stanley, Global Economic Forum, October 19, 2006, http://www.morganstanley.com/views/gef/archive/2006/20061019-Thu.html.

[17]. John Sfakianakis, “Why Saudi Arabia is Right Not to Revalue,” Financial Times, October 11, 2007, p. 11, http://www.ft.com/cms/s/2/92d94ba6-24e4-11d8-81c6-08209b00dd01,print=ye….

[18]. For a description and examples of the trilemma problem see Michael Frenkel and Lukas Menkhoff, “An Analysis of Competing IMF Reform Proposals,” Intereconomics, May/June 2000, pp. 107-113.

[19]. “Countdown to Lift-Off,” The Economist, November 22, 2007, http://www.economist.com/finance/displaystory.cfm?story_id=10191717.

[20]. Serhan Cevik, “Pegged Pains,” Morgan-Stanley Global Economic Forum, February 20, 2007, http://www.morganstanley.com/views/gef/archive/2007/20070220-Tue.html#a….

[21]. Cevik, “Pegged Pains.”

[22]. Sedat Dizmen, “An Outlook to Upcoming GCC Monetary Union’s Obstacles,” Gulf investment House, December 12, 2006.

[23]. “Qatar: To Peg or Not to Peg,” Oxford Business Group, December 10, 2007.

[24]. “Qatar: To Peg or Not to Peg.”

[25]. Setser, The Case for Exchange Rate Flexibility in Oil-Exporting Economies.

[26]. Setser, The Case for Exchange Rate Flexibility in Oil-Exporting Economies, pp. 3-4.

[27]. For a discussion of the dollar zone and its implications for the international value see Robert Looney, “The Iranian Oil Bourse: A Threat to Dollar Supremacy?” Challenge, Vol. 50, No. 2, March/April 2007, pp. 86-109, http://web.nps.navy.mil/~relooney/Rel-Challenge-07.pdf.

[28]. “Countdown to Lift-Off,” The Economist, November 22, 2007.

[29]. Stephen Jen and Charles St-Arnaud, “A Managed Float is the Ultimate Goal for the GCC,” Morgan Stanley Global Economic Forum, November 23, 2007, http://www.morganstanley.com/views/gef/archive/2007/20071123-Fri.html#a….

[30]. Lidstone, “Fixed Ideas,” pp. 4-5.

[31]. “Dollar Likely to Remain Resilient,” Oxford Analytica, May 30, 2006.

[32]. Lidstone, “Fixed Ideas,” pp. 4-5.

The Middle East Institute (MEI) is an independent, non-partisan, non-for-profit, educational organization. It does not engage in advocacy and its scholars’ opinions are their own. MEI welcomes financial donations, but retains sole editorial control over its work and its publications reflect only the authors’ views. For a listing of MEI donors, please click here.